Arbeitspapier

Income underreporting based on income expenditure gaps: Survey vs tax records

We estimate the extent of income underreporting among working households, using data from an income survey linked with individual tax records for Estonia. Income underreporting is inferred from consumption propensities, following and extending the method by Pissarides andWeber (1989). Our dataset allows us to assess the validity of the key assumption in related studies that survey income corresponds to income reported to the tax authority. Our results show large underreporting of earnings by the self-employed and also substantial underreporting of earnings by private sector employees on the basis of register income, while a much smaller scale of non-compliance is detected for self-employed and no underreporting for private employees using survey incomes. This suggests that previous studies applying this methodology to survey data have underestimated the extent of non-compliance.

- Sprache

-

Englisch

- Erschienen in

-

Series: ISER Working Paper Series ; No. 2015-15

- Klassifikation

-

Wirtschaft

Tax Evasion and Avoidance

Fiscal Policies and Behavior of Economic Agents: Household

- Thema

-

tax compliance

tax reports

income survey

expenditure

Estonia

- Ereignis

-

Geistige Schöpfung

- (wer)

-

Paulus, Alari

- Ereignis

-

Veröffentlichung

- (wer)

-

University of Essex, Institute for Social and Economic Research (ISER)

- (wo)

-

Colchester

- (wann)

-

2015

- Handle

- Letzte Aktualisierung

- 10.03.2025, 11:41 MEZ

Datenpartner

ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften - Leibniz-Informationszentrum Wirtschaft. Bei Fragen zum Objekt wenden Sie sich bitte an den Datenpartner.

Objekttyp

- Arbeitspapier

Beteiligte

- Paulus, Alari

- University of Essex, Institute for Social and Economic Research (ISER)

Entstanden

- 2015

Ähnliche Objekte (12)

The distributional effects of personal income tax expenditure

The distributional effects of personal income tax expenditure

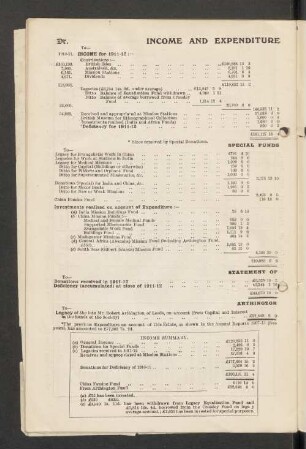

Income and expenditure

Income replacement in retirement: Longitudinal evidence from income tax records

German income tax : personal income tax, corporate income tax and trade tax

Household Expenditure and the Income Tax Rebates of 2001

Income tax buyouts and income tax evasion

Income Tax Buyouts and Income Tax Evasion

INCOME TAX

INCOME TAX

Inequality and income gaps

Capital Income Tax Coordination and the Income Tax Mix

The distributional effects of personal income tax expenditure

The distributional effects of personal income tax expenditure

Income and expenditure

Income replacement in retirement: Longitudinal evidence from income tax records

German income tax : personal income tax, corporate income tax and trade tax

Household Expenditure and the Income Tax Rebates of 2001

Income tax buyouts and income tax evasion

Income Tax Buyouts and Income Tax Evasion

INCOME TAX

INCOME TAX

Inequality and income gaps

Capital Income Tax Coordination and the Income Tax Mix

The distributional effects of personal income tax expenditure

The distributional effects of personal income tax expenditure

Income and expenditure

Income replacement in retirement: Longitudinal evidence from income tax records

German income tax : personal income tax, corporate income tax and trade tax

Household Expenditure and the Income Tax Rebates of 2001

Income tax buyouts and income tax evasion

Income Tax Buyouts and Income Tax Evasion

INCOME TAX

INCOME TAX

Inequality and income gaps