Arbeitspapier

Interest limitation rules and business cycles: Empirical evidence

This paper studies the performance of interest limita- tion rules during business cycles. It employs register data on Finnish affiliates of multinational enterprises (MNEs) to study both thin-capitalization rules (TCRs) and earnings-stripping rules (ESRs). Both types of rules are found to become tighter in economic downturns: TCRs due to higher debt-to-equity ratios and ESRs due to lower company profits. Among equally tight interest limitation rules, TCRs are found to provide less variation and less pro-cyclical outcomes by increasing the compa- ny tax burden less than ESRs in an economic downturn. While ESRs increase the tax burden of Finnish compa- nies by 17.5%-19.3% following the 2008 global financial crisis, for TCRs the increase is less than 10%. Among the ESRs, we find that an EBIT rule induces tighter tax treat- ment in economic downturns than an EBITDA rule. How- ever, the differences between ESRs remain very small.

- Language

-

Englisch

- Bibliographic citation

-

Series: ETLA Working Papers ; No. 90

- Classification

-

Wirtschaft

Business Taxes and Subsidies including sales and value-added (VAT)

Tax Evasion and Avoidance

International Business Cycles

- Subject

-

Business cycles

Corporate income taxation

Anti-tax avoidance rules

Thin-Capitalization Rules (TCRs)

Earnings Stripping Rules (ESRs)

- Event

-

Geistige Schöpfung

- (who)

-

Ropponen, Olli

- Event

-

Veröffentlichung

- (who)

-

The Research Institute of the Finnish Economy (ETLA)

- (where)

-

Helsinki

- (when)

-

2021

- Handle

- Last update

-

10.03.2025, 11:42 AM CET

Data provider

ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften - Leibniz-Informationszentrum Wirtschaft. If you have any questions about the object, please contact the data provider.

Object type

- Arbeitspapier

Associated

- Ropponen, Olli

- The Research Institute of the Finnish Economy (ETLA)

Time of origin

- 2021

Other Objects (12)

Interest limitation rule under ATAD: Case of the Czech Republi

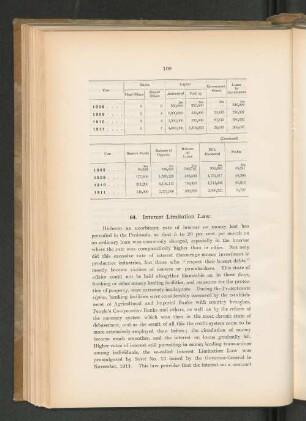

64. Interest Limitation Law.

Chaotic interest rate rules

Debt cycles with endogenous interest rate

Debt cycles with endogenous interest rate

Monetary policy, interest rate rules, and the term structure of interest rates : theoretical considerations and empirical implications

Multiple resource limitation theory applied to herbivorous consumers : Liebig's minimum rule vs. interactive co-limitation

The Golden Interest Rule: Robust Simple Interest Rate Rules for the Norwegian Economy

Business cycles and institutions : empirical analysis

Interest rate rules under financial dominance

Interest-Group Politics under Majority Rule

Backward-Looking Interest-Rate Rules, Interest-Rate Smoothing,and Macroeconomic Instability

Interest limitation rule under ATAD: Case of the Czech Republi

64. Interest Limitation Law.

Chaotic interest rate rules

Debt cycles with endogenous interest rate

Debt cycles with endogenous interest rate

Monetary policy, interest rate rules, and the term structure of interest rates : theoretical considerations and empirical implications

Multiple resource limitation theory applied to herbivorous consumers : Liebig's minimum rule vs. interactive co-limitation

The Golden Interest Rule: Robust Simple Interest Rate Rules for the Norwegian Economy

Business cycles and institutions : empirical analysis

Interest rate rules under financial dominance

Interest-Group Politics under Majority Rule

Backward-Looking Interest-Rate Rules, Interest-Rate Smoothing,and Macroeconomic Instability

Interest limitation rule under ATAD: Case of the Czech Republi

64. Interest Limitation Law.

Chaotic interest rate rules

Debt cycles with endogenous interest rate

Debt cycles with endogenous interest rate

Monetary policy, interest rate rules, and the term structure of interest rates : theoretical considerations and empirical implications

Multiple resource limitation theory applied to herbivorous consumers : Liebig's minimum rule vs. interactive co-limitation

The Golden Interest Rule: Robust Simple Interest Rate Rules for the Norwegian Economy

Business cycles and institutions : empirical analysis

Interest rate rules under financial dominance

Interest-Group Politics under Majority Rule