Arbeitspapier

The three parties in the race to the bottom : host governments, home governments and multinational companies

Most studies of tax competition and the race to the bottom focus on potential host countries competing for mobile capital, neglecting the role of corporate tax planning and of home governments that facilitate this planning. This neglect in part reflects the narrow view frequently taken of the policy instruments that countries have available in tax competition. But high-tax host governments can, for example, permit income to be shifted out to tax havens as a way of attracting mobile companies. Home countries will cooperate in this shift if their companies? gain is greater than any reduction in the domestic tax base. We use various types of U.S. data, including firm level tax files, to identify the role of the three parties (host governments, home governments and MNCs) in the evolution of tax burdens on U.S. companies abroad from 1992 to 2002. This period is of particular interest because the United States introduced regulations in 1997 that greatly simplified the use of more aggressive tax planning techniques. The evidence indicates that from 1992 to 1998 the decline in effective tax rates on U.S. companies was driven largely by host governments defending their market share. But after 1998, tax avoidance behavior seems much more important. One indication is that effective tax rates on U.S. companies had a much weaker link with local statutory tax rates. After 1997, the new regulations motivated a very large growth in intercompany payments and a parallel growth of holding company income abroad. We attempt to estimate how many of these payments were deductible in the host country, and conclude that by 2002 the companies were saving about $7.0 billion per year by using the more aggressive planning strategies. This amounts to about 4 percent of companies? foreign direct investment income and about 15 percent of their foreign tax burden.

- Sprache

-

Englisch

- Erschienen in

-

Series: CESifo Working Paper ; No. 1613

- Klassifikation

-

Wirtschaft

Business Taxes and Subsidies including sales and value-added (VAT)

State and Local Government; Intergovernmental Relations: Interjurisdictional Differentials and Their Effects

- Thema

-

Steuerwettbewerb

Unternehmensbesteuerung

Außensteuerrecht

Steuerplanung

Steuerbelastung

Multinationales Unternehmen

USA

- Ereignis

-

Geistige Schöpfung

- (wer)

-

Altshuler, Rosanne

Grubert, Harry

- Ereignis

-

Veröffentlichung

- (wer)

-

Center for Economic Studies and ifo Institute (CESifo)

- (wo)

-

Munich

- (wann)

-

2005

- Handle

- Letzte Aktualisierung

- 10.03.2025, 11:45 MEZ

Datenpartner

ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften - Leibniz-Informationszentrum Wirtschaft. Bei Fragen zum Objekt wenden Sie sich bitte an den Datenpartner.

Objekttyp

- Arbeitspapier

Beteiligte

- Altshuler, Rosanne

- Grubert, Harry

- Center for Economic Studies and ifo Institute (CESifo)

Entstanden

- 2005

Ähnliche Objekte (12)

The three parties in the race to the bottom: host governments, home governments and multinational companies

The Provincial Governments

The Provincal Governments

The Governments of the Empire.

Why do governments sell privatised companies abroad?

Dangerous Liaisons? Governments, companies and Internet governance

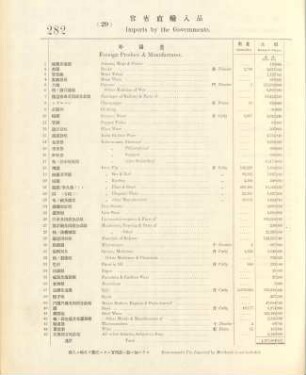

29. Imports by the governments

Green Governments

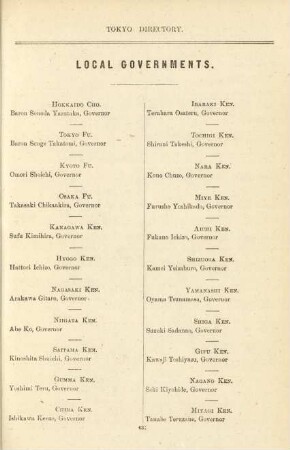

Local governments

Stable governments and the semistrict core

The Political Economy of Technocratic Governments

Governments Bad Bargains.

The three parties in the race to the bottom: host governments, home governments and multinational companies

The Provincial Governments

The Provincal Governments

The Governments of the Empire.

Why do governments sell privatised companies abroad?

Dangerous Liaisons? Governments, companies and Internet governance

29. Imports by the governments

Green Governments

Local governments

Stable governments and the semistrict core

The Political Economy of Technocratic Governments

Governments Bad Bargains.

The three parties in the race to the bottom: host governments, home governments and multinational companies

The Provincial Governments

The Provincal Governments

The Governments of the Empire.

Why do governments sell privatised companies abroad?

Dangerous Liaisons? Governments, companies and Internet governance

29. Imports by the governments

Green Governments

Local governments

Stable governments and the semistrict core

The Political Economy of Technocratic Governments