Arbeitspapier

A note on reliefs for traveling expenses to work

Assuming that higher traveling expenses reduce traveling time, this paper considers reliefs for traveling expenses to work when a distorting wage tax is levied. While the decision on traveling expenses would not be distorted if traveling costs were completely deductible, taxation would still not be neutral with respect to the leisure-consumption choice. Moreover, the paper shows that second-best optimum taxation requires less than complete deductibility of traveling expenses to work.

- ISBN

-

3931052117

- Sprache

-

Englisch

- Erschienen in

-

Series: BERG Working Paper Series on Government and Growth ; No. 30

- Klassifikation

-

Wirtschaft

Taxation and Subsidies: Efficiency; Optimal Taxation

Personal Income and Other Nonbusiness Taxes and Subsidies; includes inheritance and gift taxes

- Thema

-

income taxation

reliefs

traveling expenses to work

optimum taxation

Kosten

Steuerbegünstigung

Lohnsteuer

Optimale Besteuerung

Theorie

Pendelverkehr

- Ereignis

-

Geistige Schöpfung

- (wer)

-

Wrede, Matthias

- Ereignis

-

Veröffentlichung

- (wer)

-

Bamberg University, Bamberg Economic Research Group on Government and Growth (BERG)

- (wo)

-

Bamberg

- (wann)

-

1999

- Handle

- Letzte Aktualisierung

-

10.03.2025, 11:41 MEZ

Datenpartner

Dieses Objekt wird bereitgestellt von:

ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften - Leibniz-Informationszentrum Wirtschaft. Bei Fragen zum Objekt wenden Sie sich bitte an den Datenpartner.

ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften - Leibniz-Informationszentrum Wirtschaft. Bei Fragen zum Objekt wenden Sie sich bitte an den Datenpartner.

Objekttyp

- Arbeitspapier

Beteiligte

- Wrede, Matthias

- Bamberg University, Bamberg Economic Research Group on Government and Growth (BERG)

Entstanden

- 1999

Ähnliche Objekte (12)

A note on reliefs for traveling expenses to work

Mobility and reliefs for traveling expenses to work

Mobility and reliefs for traveling expenses to work

Expenses.

MESS EXPENSES

Efficiency effects of tax deductions for work-related expenses

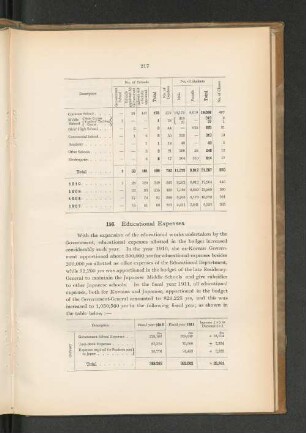

156. Educational Expenses.

EXPENSES OF SEMINARS

17. Local Governments Expenses.

11. Local Government Expenses.

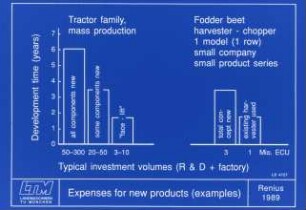

Expenses for products (examples)

Complexity and Progressivity in Income Tax Design : Deductions for Work-Related Expenses

A note on reliefs for traveling expenses to work

Mobility and reliefs for traveling expenses to work

Mobility and reliefs for traveling expenses to work

Expenses.

MESS EXPENSES

Efficiency effects of tax deductions for work-related expenses

156. Educational Expenses.

EXPENSES OF SEMINARS

17. Local Governments Expenses.

11. Local Government Expenses.

Expenses for products (examples)

Complexity and Progressivity in Income Tax Design : Deductions for Work-Related Expenses

A note on reliefs for traveling expenses to work

Mobility and reliefs for traveling expenses to work

Mobility and reliefs for traveling expenses to work

Expenses.

MESS EXPENSES

Efficiency effects of tax deductions for work-related expenses

156. Educational Expenses.

EXPENSES OF SEMINARS

17. Local Governments Expenses.

11. Local Government Expenses.

Expenses for products (examples)