Arbeitspapier

The empirics of Canadian government securities yields

Keynes argued that the short-term interest rate is the main driver of the long-term interest rate. This paper empirically models the relationship between short-term interest rates and long-term government securities yields in Canada, after controlling for other important financial variables. The statistical analysis uses high-frequency daily data from 1990 to 2018. It applies both the cointegration technique and Granger causality within the vector error correction (VEC) framework. The empirical results suggest that the action of the monetary authority is an important determinant of Canadian government securities yields, which supports the Keynesian perspective. These findings have important implications for investors, financial analysts, and policymakers.

- Language

-

Englisch

- Bibliographic citation

-

Series: Working Paper ; No. 944

- Classification

-

Wirtschaft

Interest Rates: Determination, Term Structure, and Effects

Monetary Policy, Central Banking, and the Supply of Money and Credit: General

Macroeconomic Policy, Macroeconomic Aspects of Public Finance, and General Outlook: General

General Financial Markets: General (includes Measurement and Data)

Asset Pricing; Trading Volume; Bond Interest Rates

- Subject

-

Canadian Government Bond Yields

Long-Term Interest Rate

Short-TermInterest Rate

Monetary Policy

Cointegration

Granger Causality

- Event

-

Geistige Schöpfung

- (who)

-

Akram, Tanweer

Das, Anupam

- Event

-

Veröffentlichung

- (who)

-

Levy Economics Institute of Bard College

- (where)

-

Annandale-on-Hudson, NY

- (when)

-

2020

- Handle

- Last update

- 10.03.2025, 11:44 AM CET

Data provider

ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften - Leibniz-Informationszentrum Wirtschaft. If you have any questions about the object, please contact the data provider.

Object type

- Arbeitspapier

Associated

- Akram, Tanweer

- Das, Anupam

- Levy Economics Institute of Bard College

Time of origin

- 2020

Other Objects (12)

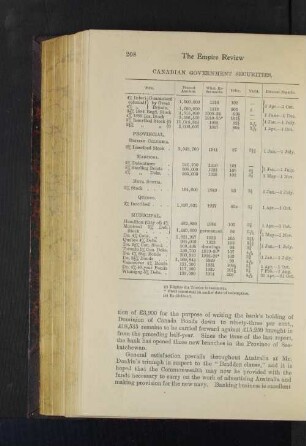

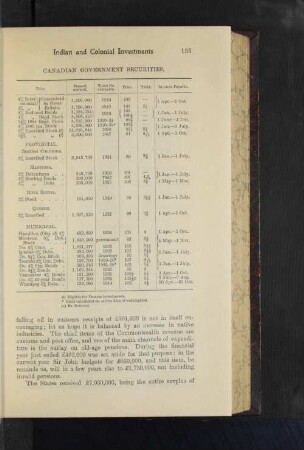

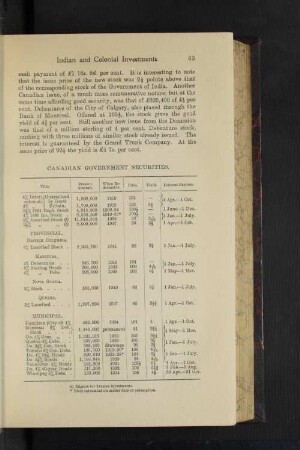

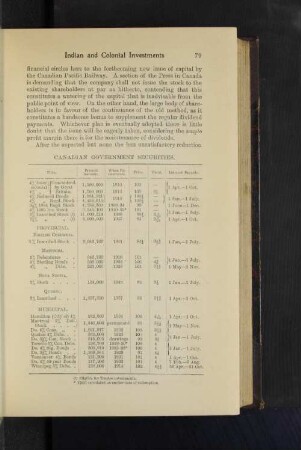

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities

Canadian Government Securities