Artikel

Combining a matheuristic with simulation for risk management of stochastic assets and liabilities

Specially in the case of scenarios under uncertainty, the efficient management of risk when matching assets and liabilities is a relevant issue for most insurance companies. This paper considers such a scenario, where different assets can be aggregated to better match a liability (or the other way around), and the goal is to find the asset-liability assignments that maximises the overall benefit over a time horizon. To solve this stochastic optimisation problem, a simulation-optimisation methodology is proposed. We use integer programming to generate efficient asset-to-liability assignments, and Monte-Carlo simulation is employed to estimate the risk of failing to pay due liabilities. The simulation results allow us to set a safety margin parameter for the integer program, which encourage the generation of solutions satisfying a minimum reliability threshold. A series of computational experiments contribute to illustrate the proposed methodology and its utility in practical risk management.

- Sprache

-

Englisch

- Erschienen in

-

Journal: Risks ; ISSN: 2227-9091 ; Volume: 8 ; Year: 2020 ; Issue: 4 ; Pages: 1-14 ; Basel: MDPI

- Klassifikation

-

Wirtschaft

- Thema

-

assets and liabilities management

risk management

uncertainty

matheuristics

simulation

- Ereignis

-

Geistige Schöpfung

- (wer)

-

Bayliss, Christopher

Serra, Marti

Nieto, Armando

Juan, Angel A.

- Ereignis

-

Veröffentlichung

- (wer)

-

MDPI

- (wo)

-

Basel

- (wann)

-

2020

- DOI

-

doi:10.3390/risks8040131

- Handle

- Letzte Aktualisierung

-

10.03.2025, 11:42 MEZ

Datenpartner

ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften - Leibniz-Informationszentrum Wirtschaft. Bei Fragen zum Objekt wenden Sie sich bitte an den Datenpartner.

Objekttyp

- Artikel

Beteiligte

- Bayliss, Christopher

- Serra, Marti

- Nieto, Armando

- Juan, Angel A.

- MDPI

Entstanden

- 2020

Ähnliche Objekte (12)

Alternative assets and cryptocurrencies

Alternative assets and cryptocurrencies

On the diversification of fixed income assets

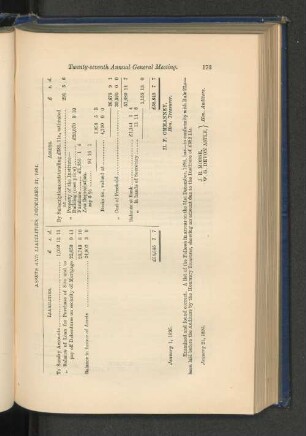

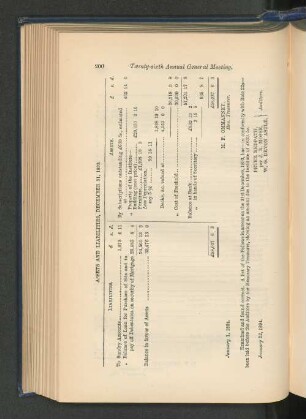

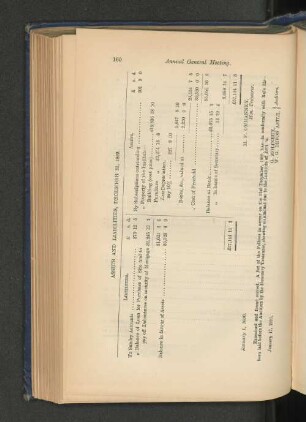

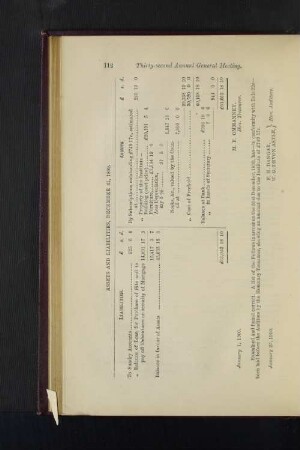

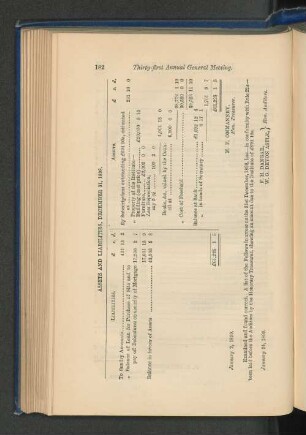

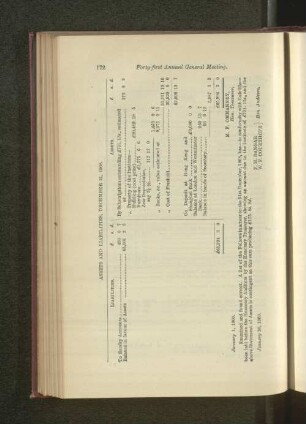

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statements of Assets and Liabilities.

Statements of Assets and Liabilities.

Statement of Assets and Liabilities.

Alternative assets and cryptocurrencies

Alternative assets and cryptocurrencies

On the diversification of fixed income assets

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statements of Assets and Liabilities.

Statements of Assets and Liabilities.

Statement of Assets and Liabilities.

Alternative assets and cryptocurrencies

Alternative assets and cryptocurrencies

On the diversification of fixed income assets

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statement of Assets and Liabilities.

Statements of Assets and Liabilities.

Statements of Assets and Liabilities.