Konferenzbeitrag

Predicting Monetary Policy Using Artificial Neural Networks

This paper analyses the forecasting performance of monetary policy reaction functions using U.S. Federal Reserve's Greenbook real-time data. The results indicate that articial neural networks are able to predict the nominal interest rate better than linear and nonlinear Taylor rule models as well as univariate processes. While in-sample measures usually imply a forward-looking behaviour of the central bank, using nowcasts of the explanatory variables seems to be better suited for forecasting purposes. Overall, evidence suggests that U.S. monetary policy behaviour between 1987-2012 is nonlinear.

- Sprache

-

Englisch

- Erschienen in

-

Series: Beiträge zur Jahrestagung des Vereins für Socialpolitik 2019: 30 Jahre Mauerfall - Demokratie und Marktwirtschaft - Session: Econometrics - Forecasting I ; No. B07-V3

- Klassifikation

-

Wirtschaft

Neural Networks and Related Topics

Forecasting Models; Simulation Methods

Money and Interest Rates: Forecasting and Simulation: Models and Applications

- Ereignis

-

Geistige Schöpfung

- (wer)

-

Hinterlang, Natascha

- Ereignis

-

Veröffentlichung

- (wer)

-

ZBW - Leibniz-Informationszentrum Wirtschaft

- (wo)

-

Kiel, Hamburg

- (wann)

-

2019

- Handle

- Letzte Aktualisierung

- 10.03.2025, 11:41 MEZ

Datenpartner

Dieses Objekt wird bereitgestellt von:

ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften - Leibniz-Informationszentrum Wirtschaft. Bei Fragen zum Objekt wenden Sie sich bitte an den Datenpartner.

ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften - Leibniz-Informationszentrum Wirtschaft. Bei Fragen zum Objekt wenden Sie sich bitte an den Datenpartner.

Objekttyp

- Konferenzbeitrag

Beteiligte

- Hinterlang, Natascha

- ZBW - Leibniz-Informationszentrum Wirtschaft

Entstanden

- 2019

Ähnliche Objekte (12)

Predicting monetary policy using artificial neural networks

Artificial neural networks for predicting real estate prices

Inclusive Multiple Model Using Hybrid Artificial Neural Networks for Predicting Evaporation

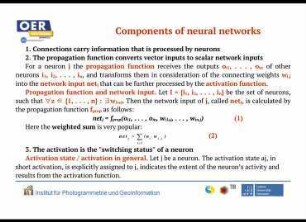

Components of artificial neural networks

Artificial neural networks, Pt. 1

Artificial neural networks, Pt. 2

Artificial neural networks, Pt. 1

Artificial neural networks, Pt. 2

Artificial neural networks, Pt. 1

Artificial neural networks in biomedicine

Artificial neural networks, Pt. 3

Artificial neural networks, Pt. 2

Predicting monetary policy using artificial neural networks

Artificial neural networks for predicting real estate prices

Inclusive Multiple Model Using Hybrid Artificial Neural Networks for Predicting Evaporation

Components of artificial neural networks

Artificial neural networks, Pt. 1

Artificial neural networks, Pt. 2

Artificial neural networks, Pt. 1

Artificial neural networks, Pt. 2

Artificial neural networks, Pt. 1

Artificial neural networks in biomedicine

Artificial neural networks, Pt. 3

Artificial neural networks, Pt. 2

Predicting monetary policy using artificial neural networks

Artificial neural networks for predicting real estate prices

Inclusive Multiple Model Using Hybrid Artificial Neural Networks for Predicting Evaporation

Components of artificial neural networks

Artificial neural networks, Pt. 1

Artificial neural networks, Pt. 2

Artificial neural networks, Pt. 1

Artificial neural networks, Pt. 2

Artificial neural networks, Pt. 1

Artificial neural networks in biomedicine

Artificial neural networks, Pt. 3